Wrapping up a solid 2025 campaign led by healthy demand for Titleist balls and golf clubs, David Maher, president and CEO at Acushnet Holdings Corp., provided an upbeat outlook for 2026, stating that he is “optimistic about the structural health of the golf industry” and sees new product pipelines fueling continued momentum across the Titleist business while strengthening its FootJoy business.

The company’s sales forecast calls for increases of 2.5 percent and 4.5 percent in the current year, on top of a 4.1 percent gain in 2025.

The sales gains in 2025 were driven by higher net sales in Titleist golf equipment, primarily from higher average selling prices in golf clubs and higher sales volumes in golf balls, as well as higher net sales in golf gear, primarily from higher average selling prices across all product categories. These increases were partially offset by lower net sales in FootJoy golf wear, primarily due to lower footwear sales volumes, partially offset by higher average selling prices across all product categories. An increase in net sales of products not allocated to one of its three reportable segments also contributed to the change in net sales.

Maher said the game of golf’s increased momentum is evident with worldwide rounds projected to increase about 2 percent in 2026, driven by growth in EMEA, the U.S., and Japan, and a flat year in Korea.

“In the U.S., our largest market, the number of golfers again increased, contributing to the rounds of play momentum,” added Maher. “The global golf industry, as defined by golf courses, teaching centers and golf retailers, continues to be healthy, with strong financials supporting ongoing investments as the industry adapts to meet ever-evolving golfer preferences.”

Within Acushnet, Maher cited several launches planned to help “sustain the momentum our brands carry into 2026.”

On the hard lines side, as is customary in even-numbered years, new Titleist Golf Balls were launched in the first quarter, including Pro V1x Left Dash and new AVX Tour Soft and Velocity models. At Titleist Golf Clubs, the new Vokey SM11 wedges and a new lineup of Scotty Cameron Mallet Putters, (shown lead photo), are launching in Q1. Said Maher, “Both products debuted on worldwide tours earlier this year, and initial responses have met our very high expectations.”

Maher added that a new driver launch is scheduled for late June, earlier than its customary Q3 timing, as the brands look to capitalize on Titleist’s position as the number one driver on the PGA Tour. The CEO said, “We are enthused by the great work from our product development and operations teams to provide added flexibility around launch timing.”

He said the overall Titleist golf equipment business continues to benefit from investments in R&D, operational efficiencies, and capacity expansion that have helped drive innovation.

Acushnet’s gear business (golf bags, headwear, gloves, travel gear, and other accessories) “is well positioned, coming off a strong 2025,” according to Maher. Growth in the gear business is expected to be led by gains in the U.S. and EMEA.

Maher said FootJoy “continues to move forward in 2026 as we leverage high-performance Premiere and Pro/SL franchises to strengthen our position as the number one shoe in golf. We continually evolve our outerwear and apparel offerings with a focus on our premium segments as we position FJ for the future and manage near-term tariff headwinds.”

Summary of Full Year 2025 Financial Results

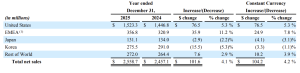

Acushnet’s sales for the year increased 4.1 percent, or 4.2 percent on a constant-currency basis, to $2.56 billion, topping company guidance that called for sales in the range of $2.52 billion to $2.54 billion.

Net income declined 12.0 percent to $188.5 million, down 12.0 percent year-over-year, primarily driven by a $17.0 million loss on debt extinguishment related to its 2025 debt refinancing, an increase in interest expense, net, and lower income from operations, partially offset by a noncash pre-tax gain of $20.9 million related to the deconsolidation of its FootJoy golf shoe joint venture.

Adjusted EBITDA was $410.4 million, up 1.5 percent year over year. EBITDA landed at the mid-point of the guidance range between $405 to $415 million. Adjusted EBITDA margin was 16.0 percent versus 16.5 percent for the prior year period.

On a geographic basis, higher net sales in the United States were largely driven by increases in Titleist golf equipment of $60.8 million and golf gear of $9.4 million. The increase in Titleist golf equipment was primarily driven by higher average selling prices for golf clubs and higher sales volumes of its 2025 Pro V1 golf ball models, GT hybrids, and its latest-generation T-Series irons. These increases were partially offset by lower sales volumes of second model year GT drivers, SM10 wedges, and performance model golf balls. The increase in golf gear was primarily driven by higher average selling prices across all product categories. An increase in net sales of products not allocated to any of the three reportable segments also contributed to the change in net sales.

Net sales in regions outside the U.S. were up 2.5 percent, or 2.7 percent on a constant-currency basis, driven by increases in EMEA and Rest of World, partially offset by decreases in Japan and Korea. In EMEA and Rest of World, the increases were driven by higher net sales across all reportable segments. An increase in net sales of products not allocated to any of its three reportable segments also contributed to the change in net sales in Rest of World. In Japan, the decrease was primarily due to lower net sales in FootJoy golf wear, largely in footwear and apparel, partially offset by higher net sales in Titleist golf equipment, driven by golf balls. In Korea, the decrease was largely due to lower net sales in FootJoy golf wear, primarily in the footwear and apparel product categories, and in golf gear, partially offset by higher net sales in Titleist golf equipment, largely driven by golf clubs.

Segment Specifics

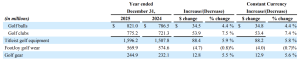

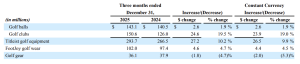

5.9 percent increase in net sales (5.8 percent on a constant currency basis) of Titleist golf equipment, primarily driven by higher average selling prices in golf clubs and sales volumes of its 2025 Pro V1 golf ball models. In addition, higher sales volumes of its latest-generation T-Series irons and GT hybrids were more than offset by lower sales volumes of its second-year drivers, wedges, and performance-model golf balls.

0.8 percent decrease in net sales (0.7 percent on a constant currency basis) of FootJoy golf wear due to lower sales volumes, primarily in footwear, partially offset by higher average selling prices across all product categories.

5.5 percent increase in net sales (5.6 percent on a constant currency basis) of golf gear, driven by higher average selling prices across all product categories.

Maher said the Titleist golf equipment gains reflect the benefits of investments in product development and recent capacity expansion projects, which will continue with a focus on cast urethane golf ball production and custom golf club assembly.

On the ball side, the new Pro V1 posted gains across all regions, while increasing demand is being seen for Titleist’s AIM (Alignment Integrated Marking) balls. Said Maher, “Operationally, we continue to benefit from the expansion of our automated custom imprinting capabilities, which is driving efficiencies and reducing lead times.”

In golf clubs, growth was boosted by the launch of the new T-Series irons, “steady growth” in metals and Scotty Cameron putters, and “strong results” at the Vokey Wedge in year two of the SM10 product cycle. Said Maher, “Ongoing investments in product development and our global club fitting network frame how we characterize the Titleist Golf Club opportunity.”

The Titleist gear business saw “especially strong increases “in EMEA and the U.S., with growing momentum for Club Glove travel products.

FootJoy’s sales were down 1 percent, mainly due to lower discounted sales compared with last year. Said Maher, “On the strength of products like Premiere and HyperFlex, we are seeing a favorable mix shift towards our premium high-performance footwear franchises, and the FJ Mobile Fit Lab program is delivering a value-added fitting experience, which helps golfers select the best footwear, performance, and comfort option for their games. Growth in gloves and apparel added to FootJoy’s momentum and improved profitability for the year.”

KJUS, Acushnet’s ski brand, grew sales by 9 percent for the year, led by double-digit gains in the U.S. Titleist Apparel also delivered a “promising year,” led by growth in China and Korea.

Summary of Fourth Quarter 2025 Financial Results

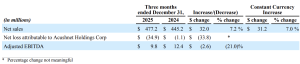

Consolidated net sales for the quarter increased 7.2 percent, or 7.0 percent on a constant-currency basis, primarily due to higher sales volumes in Titleist golf equipment, driven by golf clubs, and higher average selling prices across all reportable segments, partially offset by lower sales volumes in golf gear.

Net loss for the quarter was $34.9 million, compared to a loss of $1.1 million for the same period in 2024. This decrease was primarily driven by a $17.0 million loss on debt extinguishment related to its 2025 debt refinancing, an increase in loss from operations, and an increase in income tax benefit, offset in part by an increase in loss from operations.

Adjusted EBITDA was $9.8 million, compared to $12.4 million in the prior year. Adjusted EBITDA margin was 2.1 percent for the fourth quarter versus 2.8 percent for the prior year period.

Gross margin fell to 47.7 percent, down 60 basis points from last year, primarily related to incremental tariff costs of approximately $30 million. SG&A expense of $206 million in the quarter increased $13 million compared to the fourth quarter of 2024.

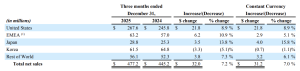

On a geographic basis, net sales in the United States were higher, primarily due to increases of $16.3 million in Titleist golf equipment and $5.5 million in FootJoy golf wear. The increase in Titleist golf equipment was primarily driven by higher sales volumes of its latest-generation T-Series irons and second model-year wedges, partially offset by lower sales volumes of second-model-year GT drivers. The increase in FootJoy golf wear was largely due to higher average selling prices, particularly in footwear.

Net sales in regions outside the United States were up 5.1 percent, or 4.7 percent on a constant currency basis, driven by increases in Japan, Rest of World, and EMEA, partially offset by a decrease in Korea. In Japan, net sales increased primarily due to higher net sales of Titleist golf equipment and products that are not allocated to one of the three reportable segments. In Rest of World, net sales increased mainly due to higher net sales of Titleist golf equipment, driven by golf clubs. In EMEA, the increase was primarily due to higher net sales of Titleist golf equipment, driven by golf clubs, partially offset by products that are not allocated to one of three reportable segments. In Korea, the decrease was largely related to lower net sales in FootJoy golf wear.

Segment Specifics

10.2 percent increase in net sales (9.9 percent on a constant currency basis) of Titleist golf equipment, largely due to higher sales volumes of T-Series irons launched in the third quarter of 2025 and second model year SM10 wedges, partially offset by lower sales volumes of second model year GT drivers.

4.7 percent increase in net sales (4.5 percent on a constant-currency basis) in FootJoy golf wear, primarily due to higher average selling prices in footwear.

4.7 percent decrease in net sales (5.3 percent on a constant-currency basis) of golf gear, primarily due to lower sales volumes across all product categories, partially offset by higher average selling prices across all product categories.

2026 Outlook

The company expects full-year consolidated net sales to be approximately $2,625 to $2,675 million on a reported basis, up 3.6 percent at the midpoint. On a constant-currency basis, consolidated net sales are expected to be up between 2.5 percent and 4.5 percent. Acushnet expects full-year adjusted EBITDA to be approximately $415 to $435 million, up 3.5 percent at the midpoint.

Sean Sullivan, EVP and CFO, said growth is expected across all reportable segments, as well as growth both domestically and internationally, with strength in EMEA and Rest of World markets. Acushnet continues to expect approximately $70 million of tariff costs in 2026, reflecting the tariff environment in place prior to the Supreme Court’s February 20th ruling.

Sullivan said, “While the decision impacts certain tariff programs, the timing, implementation, and durability of any changes remain uncertain. As a result, our 2026 financial guidance reflects the continued assumption of approximately $70 million of tariffs. As we gain greater clarity on the path forward, we will update you with any material changes to our outlook.”

Image courtesy Titleist (Scotty Cameron Mallet Putter)